75% of CPAs are set to retire in the coming decades, and fewer young accountants are joining the field. At the same time, the need for accounting services continues to grow, putting pressure on firms to keep up. In this situation, automation isn’t just a time-saver - it’s a necessity for maintaining service levels and supporting growth.

Old Automation’s False Promise

For years, firms have invested in automation tools that promised to simplify work. Traditional rule-based systems in accounting software automatically categorize transactions - until something unusual happens. One small exception - a new vendor or a slight change in a transaction description - sends accountants back to manual cleanup. A simple bank rule might flag every Amazon purchase as Office Supplies, yet when a company buys a laptop from Amazon, that rule misclassifies it instead of recognising it as an equipment asset. Robotic Process Automation (RPA) tries to mimic human clicks, but these bots are fragile; each time QuickBooks or a banking site updates its layout, accountants scramble to recode them. In short, traditional tools handled only the simple tasks, while the more complex ones still needed human intervention.

The Missing Ingredient: Context

What these systems fundamentally lacked was context. Accounting isn't about blindly applying rigid rules - it’s intrinsically linked to each client’s unique situation. Rules calibrated for one client often fail completely for another: a tech startup might classify cloud subscriptions as R&D expenses to maximize tax benefits, while a restaurant records identical subscriptions as ordinary operating costs. Geographic differences compound this complexity: California's generous R&D tax incentives might justify the startup's approach, whereas in Texas, with limited incentives, these expenses are simply operational costs.

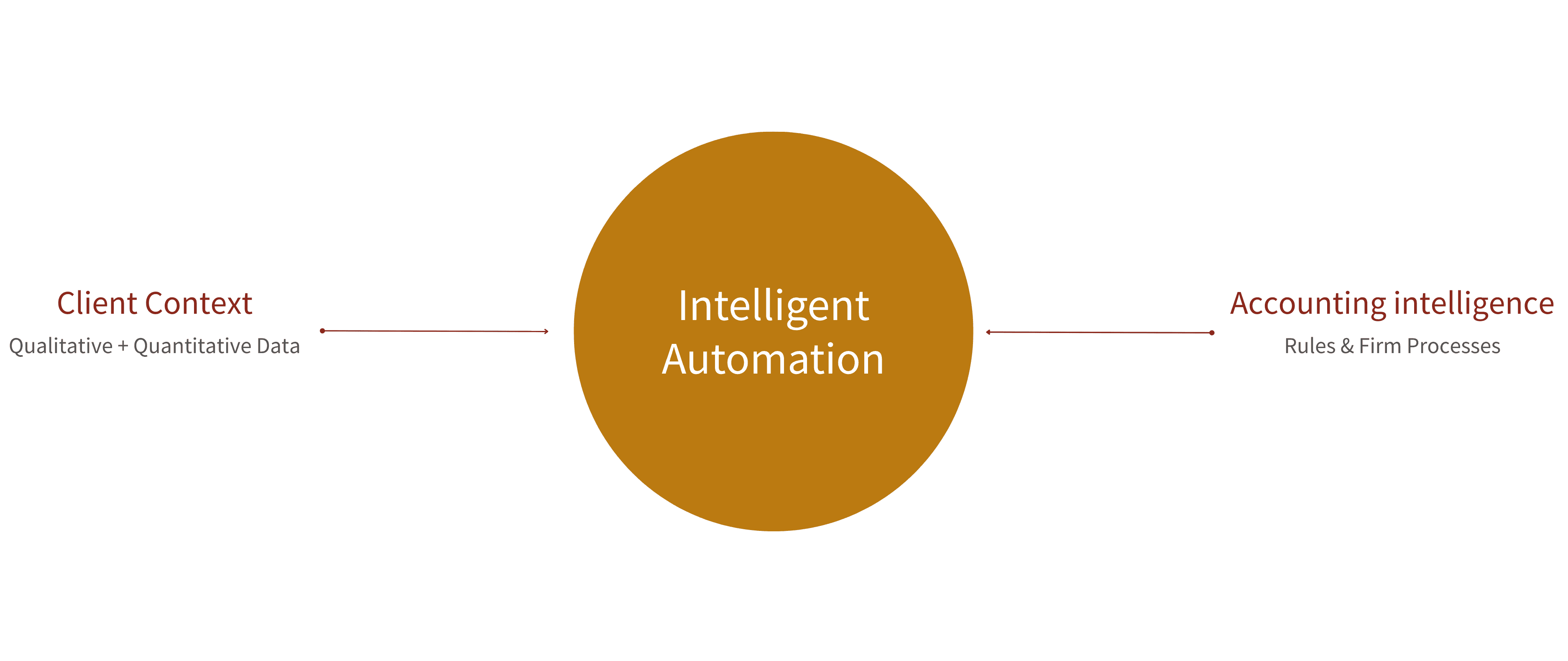

Building Intelligent Automation

To truly automate accounting workflows, tools must combine the right data with deep accounting knowledge.

1. Complete client context: The system must see the full client picture - from emails and call transcripts to ledger data, bank transactions, and key documents like contracts and receipts. This rich contextual awareness enables understanding the "who, what, and why" behind each client decision and transaction, eliminating constant manual clarification.

2. Embedded accounting intelligence: The system needs to incorporate the complex web of accounting rules, workflows, and standards that define proper practice. This includes formal guidelines (GAAP, tax codes, audit checklists) and firm-specific processes (approval workflows, internal controls). This integration ensures the system not only automates tasks but adheres to the exacting standards of accuracy and compliance that define the profession.

When these pillars converge, true end-to-end automation becomes possible, not just isolated task handling. Firms can finally scale client capacity without proportional staffing increases - while simultaneously improving quality. In an industry defined by trust, precision, and unforgiving deadlines, this represents nothing short of a paradigm shift.

AI isn't hype - it's the logical next chapter

Most accountants still view AI as distant science fiction or marketing buzz, but it's actually the natural evolution of our industry's technology adoption curve. Consider legal services - another complex, rule-bound, document-heavy profession. Legal firms have already embraced AI tools with remarkable results, leveraging language models’ capabilities perfectly aligned with their text-based workflows.

Taking the example of ChatGPT: the version you're using today will seem primitive a year from now. This pattern holds true across every AI domain. Within months, not years, AI systems will handle increasingly complex accounting workflows with surprising accuracy. Firms that resist this shift won't just be at a small disadvantage; they'll find themselves fundamentally uncompetitive in terms of both efficiency and quality. The choice isn't whether to adopt AI, but how quickly you can integrate it into your core operations before it becomes the industry standard.

Instead of treating automation as a fragile side project, it must become your number one priority - a force multiplier that truly does more with less. This means integrating AI deeply into your core operations, not just for peripheral tasks like "drafting emails with ChatGPT." This shift isn't about replacing accountants; it's about transforming their daily reality. When AI handles the repetitive, rule-driven tasks that consume most billable hours today, accountants can finally focus on what brought them to the profession: providing strategic guidance, identifying financial opportunities, and delivering genuine value to clients. The most successful accounting firms of the next decade won't just use AI tools - they'll build their entire service model around them, creating a fundamentally different kind of practice that achieves what was previously impossible: scaling high-touch professional services without proportional headcount growth.